In recent years, more couples have opted to open multiple bank accounts to help manage household finances. While there is no universal formula for how many accounts a couple should have, many find that separating spending into different categories can offer greater clarity.

This article explores common reasons couples might choose to open four accounts, typical account setups, key considerations, and some of the potential risks to be aware of.

This article is intended for general informational purposes only. It does not constitute financial advice.

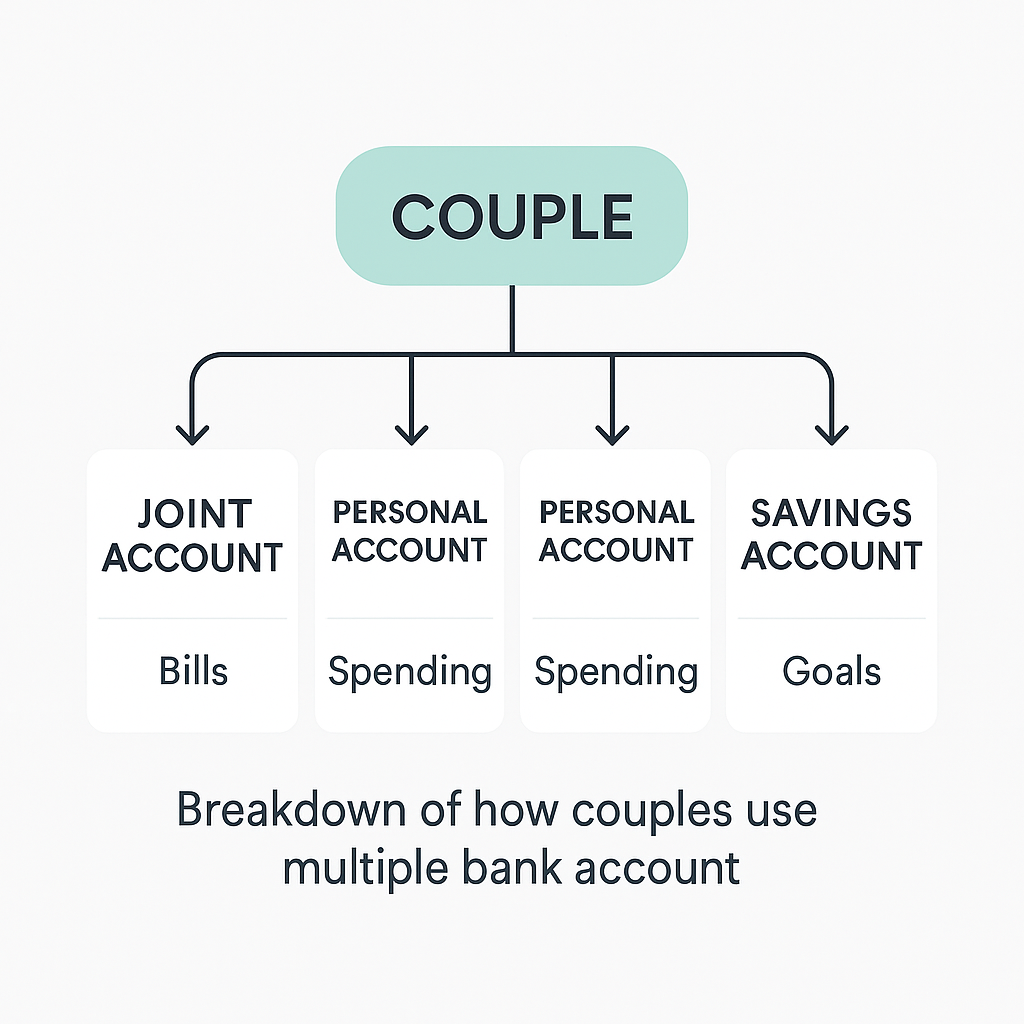

Many couples find that maintaining more than one bank account can assist with organisation, especially when managing joint expenses. Common reasons include:

Some couples say this structure promotes spending transparency and supports joint responsibility.

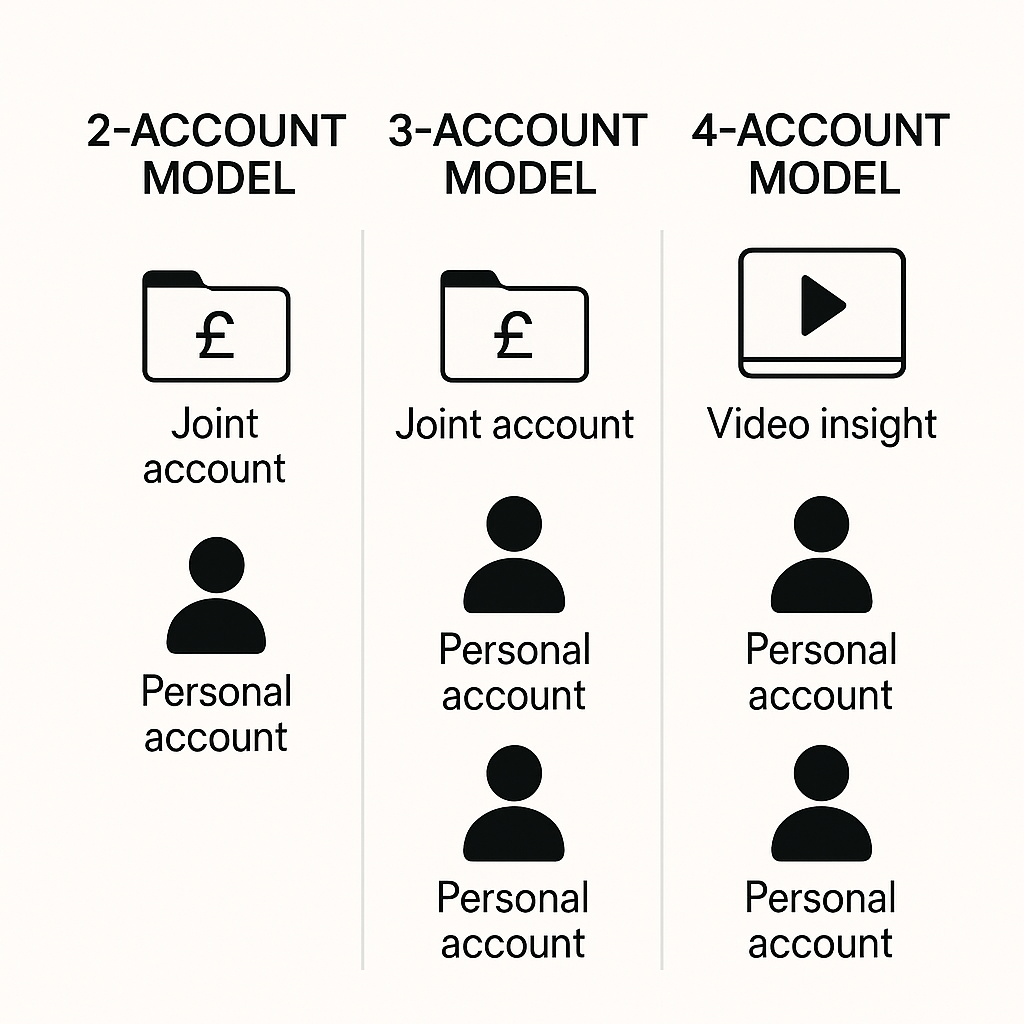

There are several popular configurations couples report using:

Public figures like Steve Harvey have discussed the four-account method, which has gained traction among couples seeking clearer financial structures. However, this is a general framework, not a recommendation.

Yes. There are no legal limits on how many bank accounts you or your partner can open in the UK. Most banks allow customers to open multiple current or savings accounts, although this is subject to identity verification and compliance checks such as Know Your Customer (KYC) procedures.

Banks may also apply fees or balance thresholds, so it’s worth checking the terms before opening new accounts.

The Financial Conduct Authority (FCA) regulates financial firms in the UK but does not set limits on the number of accounts one may have. The FCA promotes transparency and informed decision-making in financial services.

While using multiple accounts might help with financial clarity, it should not be used as a workaround for regulatory obligations or as a substitute for formal financial planning. Couples should ensure that all parties understand and agree on how each account will be used.

While multiple accounts can bring benefits, they’re not without potential downsides:

More accounts mean more to track and maintain

Some banks may charge monthly or transaction fees for certain account types

With more accounts, you increase your exposure to potential fraud or identity theft

Poor coordination could result in overdrafts or missed payments

A four-account setup can work well, but only if it’s structured, regularly reviewed, and suits both partners’ communication styles and financial habits.

Different lifestyles call for different structures. Examples include:

There’s no “correct” number of accounts. The goal is to find a setup that supports your shared financial goals.

Using tools like budgeting apps or spreadsheets can make managing several accounts easier. Features such as balance alerts and spending categories are common in apps like Monzo or Starling.

Note: These tools are mentioned for illustrative purposes only and are not endorsements.

To explore personalised budgeting strategies, you may wish to speak with an FCA-authorised adviser. Zomi Wealth offers guidance tailored to your financial circumstances.

Multiple bank accounts are one-way couples organise finances. For some, four accounts work well, but others may prefer fewer or more.

Be mindful of the added complexity, potential fees, and risks of mismanagement.

This article is for informational purposes only and should not be considered financial advice.

To explore personalised budgeting strategies, you may wish to speak with an FCA-authorised adviser. Zomi Wealth offers guidance tailored to your financial circumstances.