In the UK, many people are unclear about the difference between a financial adviser and a financial planner. These titles often sound similar, but they refer to different approaches in financial support. Understanding what each professional does can help you ask better questions and make more informed decisions.

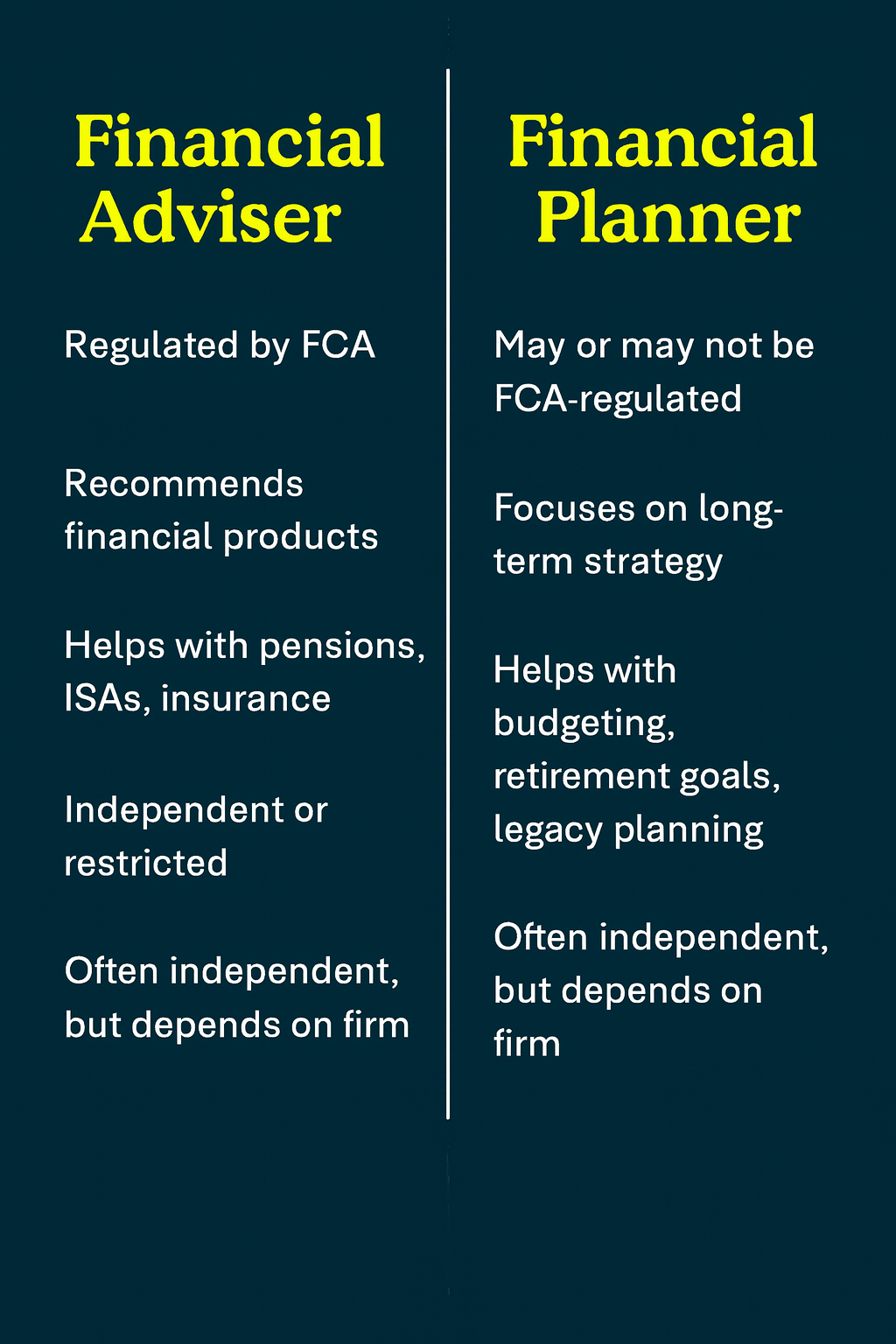

Because advisers are regulated, they are required to act in your best interests and are held accountable for their recommendations.

A financial planner helps you map out long-term financial goals, from retirement planning to tax efficiency and inheritance strategies. Planners often use tools such as cashflow modelling and scenario planning to build a personalised financial strategy.

Not all financial planners are FCA-regulated, especially if they do not provide product-specific advice. However, some are dual-qualified and act as both planners and advisers.

Their focus is more holistic and strategic, helping you structure your financial life over the long term.

While both roles deal with finances, they serve different functions:

Some professionals offer both services if they are fully qualified and regulated.

It depends on what you need:

Some professionals do both. The key is to clarify what kind of support you are seeking before committing.

A financial planner may help you:

They focus less on specific products and more on how to align your finances with your life goals. This makes planning useful for those in transition (e.g. retirement, inheritance, divorce).

Always check who you’re working with, especially if they are offering strategic advice on money.

Paying for a financial adviser can be worthwhile in situations like:

Advisers are regulated and must act in your best interest. Costs may be:

Always ask for a fee breakdown upfront.

It depends on how they work:

Earnings vary based on qualifications, clients, business model, and location.

Not exactly. Financial planning is about long-term goals and strategy. Advisory typically involves recommending regulated financial products.

They might not be FCA-regulated, services vary in quality, and they may charge fees for consultations or ongoing support.

They create long-term strategies for retirement, savings, tax efficiency, or legacy planning – often using tools like cashflow models.

It depends on your goals. Product advice? Adviser. Life strategy? Planner. Some professionals offer both services.

Yes, especially if you are planning for long-term goals like retirement or passing on wealth. Just ensure they are qualified.

You do not have to make this decision alone. At Zomi Wealth, we offer a clear, supportive space to explore your options – no advice, no pressure.

Whether you are weighing adviser vs planner or just want to talk through your options, we are here to help.