For many people approaching retirement, the idea of withdrawing a large cash amount from their pension is appealing. A pension lump sum UK withdrawal offers flexibility: you can pay off debts, support family, or reinvest elsewhere. But this decision also comes with risks, especially around taxation and long-term income security.

This guide explains the pros and cons of pension lump sums, how they are taxed, and how inflation could affect the value of your money over time.

A pension lump sum is when you withdraw part or all of your pension pot in one payment, rather than taking it as a regular income.

For example, if you have a £200,000 pension pot:

Taking a pension lump sum can be attractive for several reasons:

For some, the ability to reshape their finances immediately makes a lump sum from pension a practical choice.

However, there are also clear downsides:

In short, the pension lump sum advantages and disadvantages must be weighed carefully against your long-term retirement needs.

The rules on tax on pension lump sum UK withdrawals are strict:

Example: If you withdraw £60,000 (on top of £25,000 tax free), and your other income is £30,000, you’ll pay:

Not everyone should take their pension as a lump sum.

Inflation reduces the value of money over time.

This means your lump sum could buy less in the future unless invested in assets that keep pace with inflation.

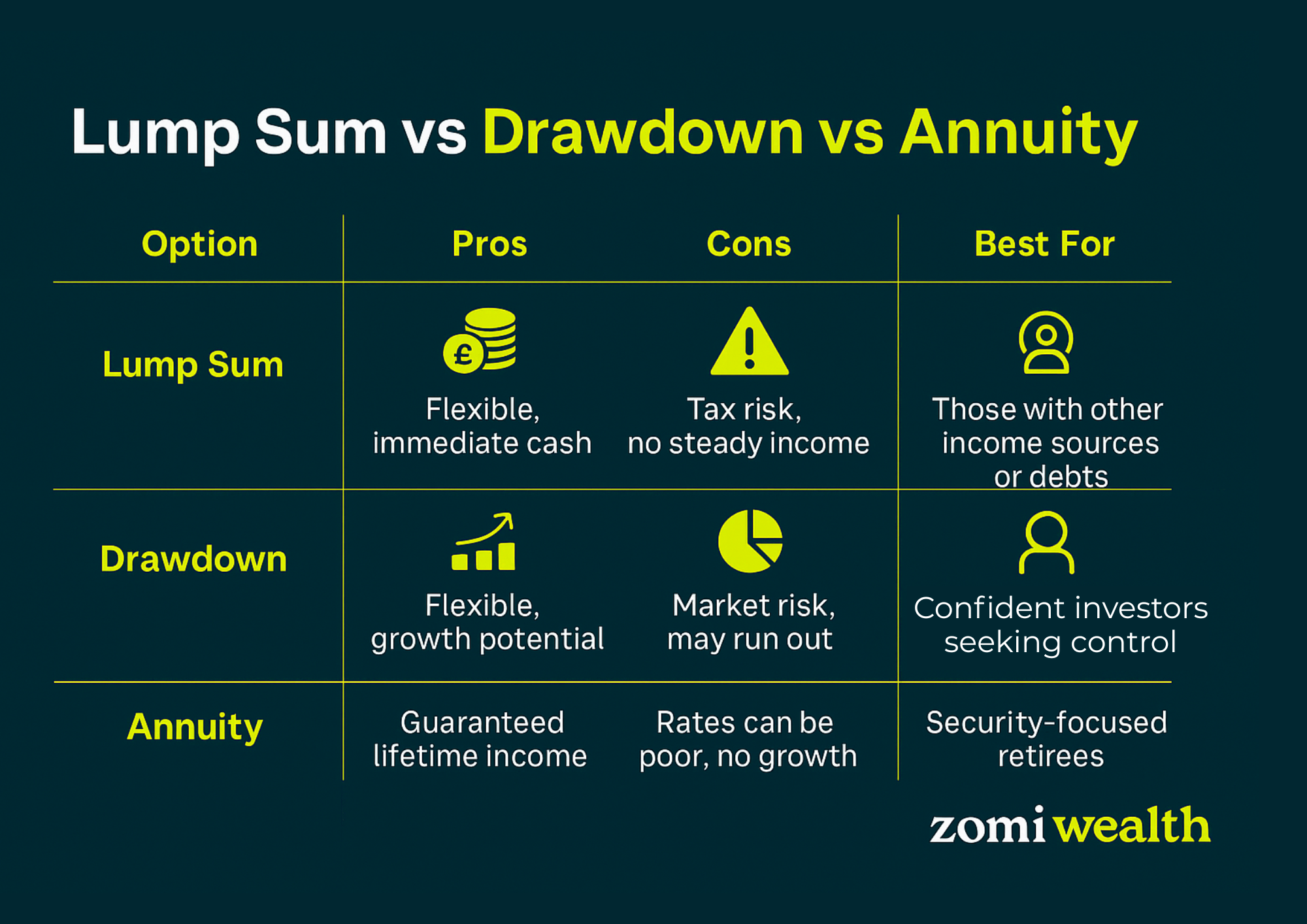

Before withdrawing everything at once, consider:

Each option has pros and cons, and often a blended approach works best.

It depends on your needs. If you need flexibility or debt repayment, it may help. But for regular income security, alternatives like drawdown or annuities may be better.

No. The 25% allowance applies to your total pension pot, not annually. Some providers allow staged withdrawals that make use of the tax-free element.

Up to 100% of your pot, but only 25% is tax free. The remainder is subject to income tax.

It’s when you take part or all of your pension as a one-off cash withdrawal instead of receiving regular income.

For more retirement planning insights, market updates, and tax-saving tips, follow Zomi Wealth on:

Stay informed and inspired as you plan your financial future.