Inflation has become one of the biggest concerns for savers and investors in the UK. Rising prices eat away at the purchasing power of your money, shaping how you save, spend, and invest.

This article explains what inflation means in investing, how it affects different asset classes, and what UK investors can do to protect their portfolios.

Inflation simply means the general rise in the price of goods and services over time. Put another way, it measures how much less you can buy with the same amount of money.

Inflation matters in investing because it acts as a silent tax. Even if your savings are “safe” in cash, their real value is shrinking if inflation outpaces interest rates.

In the UK, inflation is measured by the Office for National Statistics (ONS) using:

The Bank of England targets 2% CPI inflation. Yet the current inflation rate UK in 2025 is higher, affecting savings and investments alike.

Using a how much is money worth now calculator UK:

Tools like the UK inflation rate forecast and UK inflation history provide insight into trends and help investors plan.

Inflation doesn’t just happen – it has causes.

Understanding why inflation happens helps investors anticipate its impact.

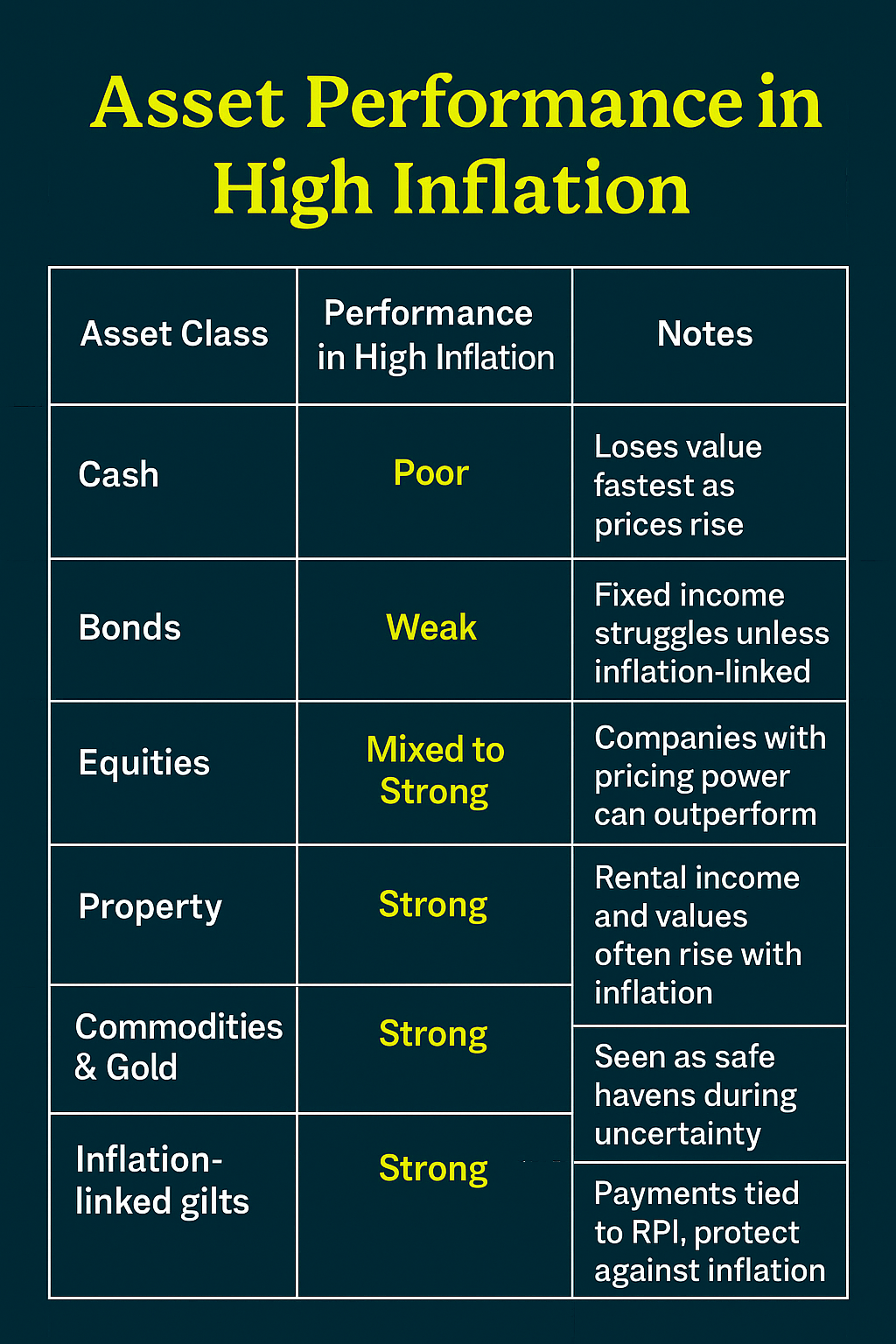

Inflation influences different investments in different ways:

So, how does inflation affect investments? It reduces real returns, but some assets, like equities and property – may benefit.

Periods of high inflation present risks but also opportunities.

So, is it good to invest during high inflation? Yes – but only in assets that can outpace rising prices. Diversification is key.

Traditional bonds are vulnerable to inflation. If you hold a bond paying 3% while inflation runs at 5%, you’re losing money in real terms.

The exception is inflation-linked gilts, which adjust payments with RPI.

Should I buy bonds when inflation rises? Only if they are inflation-linked, or if you’re balancing them with other growth assets.

One popular principle is the 10/5/3 rule of investment:

While these figures are not guaranteed, they help set realistic expectations. In the UK, actual returns may be lower depending on inflation and economic conditions.

The UK inflation forecast suggests rates may gradually move closer to the 2% Bank of England target. Yet uncertainty remains around:

For investors, this means preparing for volatility while holding assets that can withstand different scenarios.

It reduces real returns. Assets like equities and property may hold up better, while cash and bonds lose value fastest.

Yes, if you focus on assets like equities, property, and inflation-linked gilts that can outpace inflation.

It’s a guideline suggesting long-term returns of 10% for equities, 5% for bonds, and 3% for cash.

Only inflation-linked gilts make sense in such periods; fixed-rate bonds often underperform.

Some do – equities and property may increase, while bonds and cash usually fall behind.

Equities, property, inflation-linked bonds, commodities, and gold are considered good hedges.

For more retirement planning insights, market updates, and tax-saving tips, follow Zomi Wealth on:

Stay informed and inspired as you plan your financial future.