In celebration of Pension Awareness Day 2025, many are reassessing how best to convert pension savings into reliable income. The two most common options are pension annuities and income drawdown, but which is right for you?

Understanding the difference is key to long-term financial peace of mind. This guide breaks down both options, their pros and cons, and when to seek expert advice.

A pension annuity provides you with a guaranteed income for life or for a fixed term. When you buy an annuity, you exchange some (or all) of your pension pot for regular, secure income.

Annuities are low risk, ideal for those seeking financial certainty. Rates vary depending on age, health, and interest rates.

Income drawdown allows you to keep your pension invested while withdrawing income as needed. It offers more flexibility but also involves investment risk.

Ideal for those who want:

Drawdown may suit confident investors or those with other sources of income.

When planning your retirement income in the UK, one of the biggest decisions is choosing between an annuity and pension drawdown.

An annuity provides guaranteed income for life, offering long-term financial security, while income drawdown keeps your pension invested, giving you flexibility and growth potential but with added investment risk.

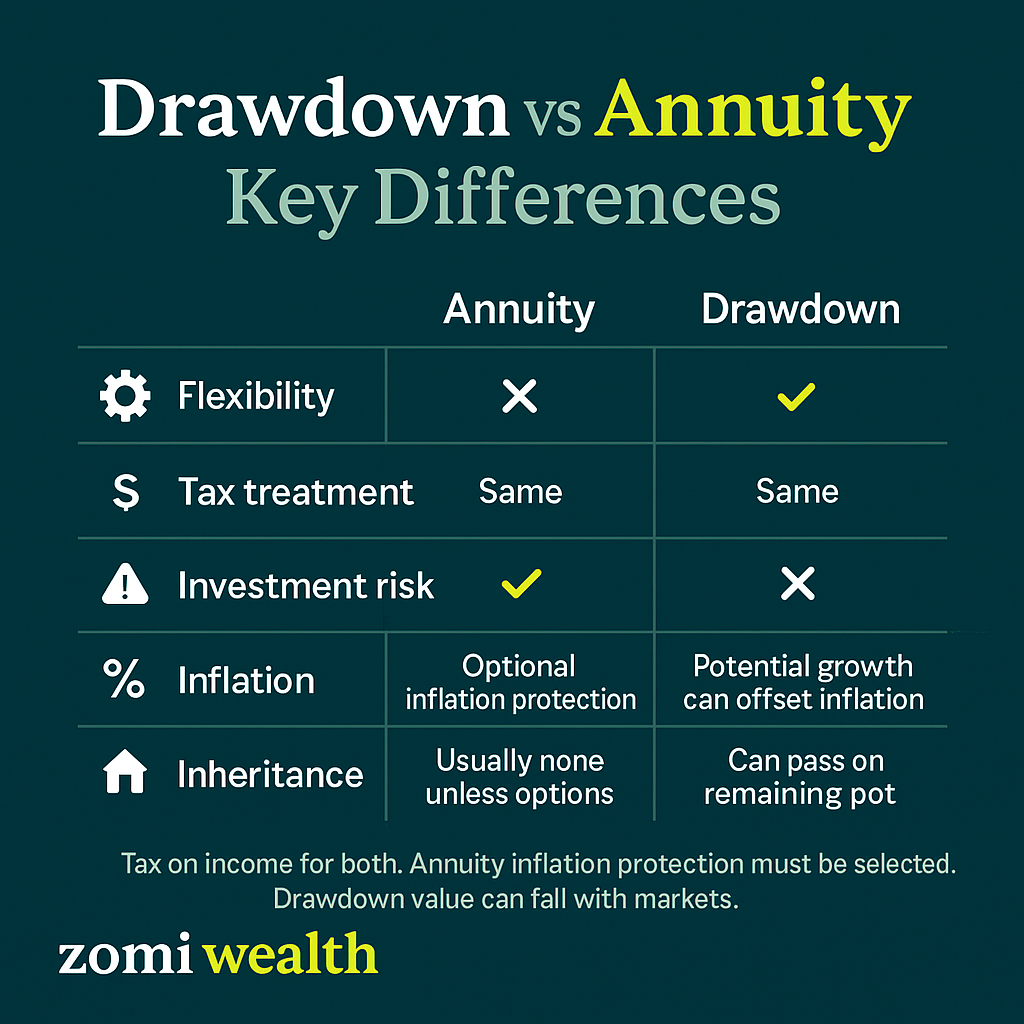

To help you decide, our annuity vs drawdown comparison table below highlights key differences in flexibility, tax treatment, inflation protection, inheritance options, and risk. Understanding these contrasts is essential for effective retirement planning and ensuring your pension pot works in line with your goals.

Use the table below to compare both pension income options at a glance:

Before choosing, consider using tools like:

These tools help you forecast retirement income under different scenarios.

A contract that provides a guaranteed income for life or a set term in exchange for a lump sum from your pension.

It lets you keep your pension invested and withdraw funds as needed, offering flexibility but with risk.

Annuity is generally safer as it offers guaranteed income. Drawdown can fluctuate based on market performance.

Yes. Some retirees choose a blended strategy—using part of their pension for an annuity and the rest in drawdown.

Use online calculators or speak to a financial adviser to model different scenarios based on your pension pot and lifestyle.

Providers like Aviva, PensionBee, and Royal London are popular in 2025. Always compare fees, flexibility, and support.

Making the right decision about your retirement income can be complex. Seeking regulated financial advice ensures your plan is tailored to your goals, tax position, and risk appetite.