Download your checklist!

Send

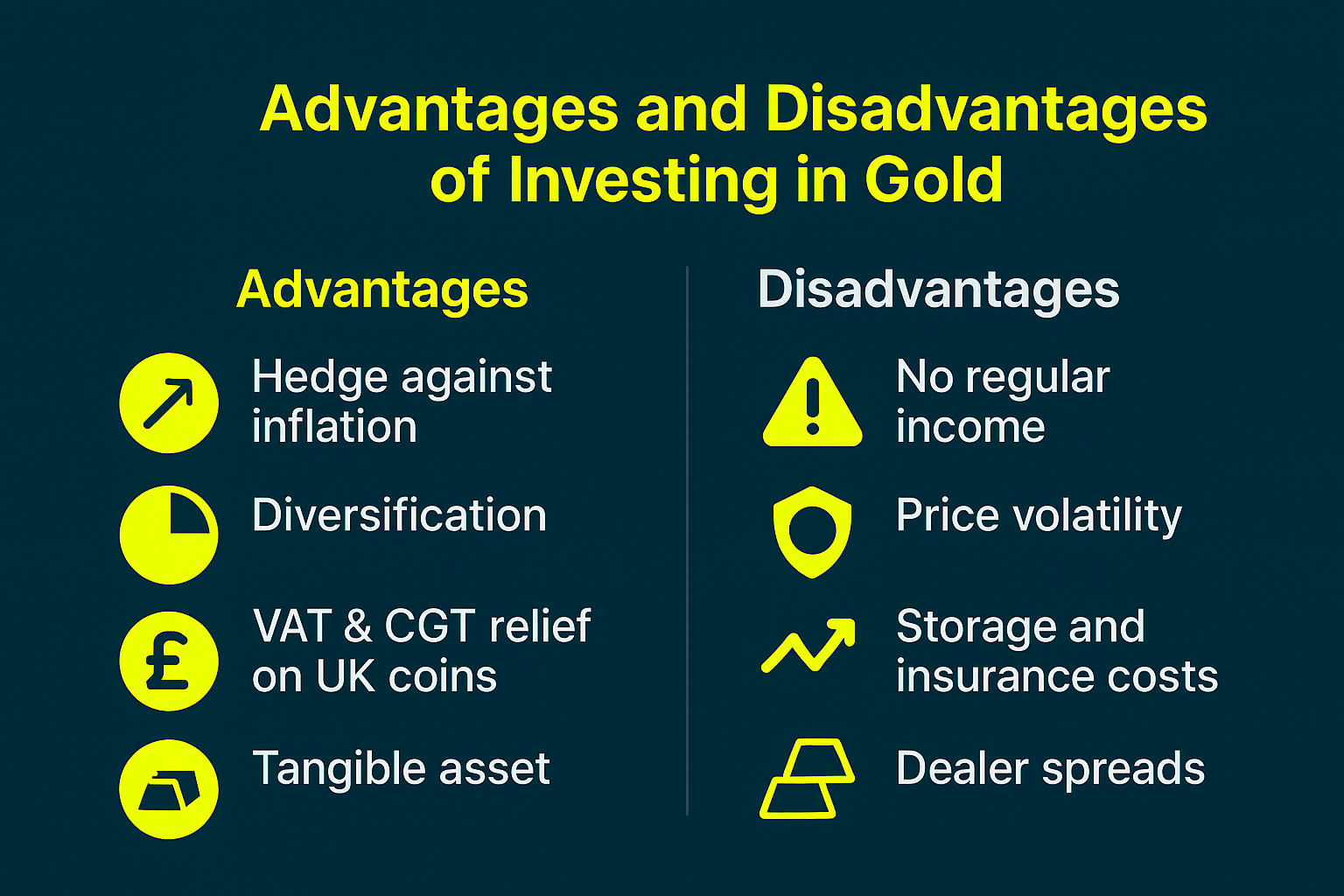

Pros: Tangible ownership, potential tax exemptions, no counterparty risk.

Cons: Requires secure storage and insurance.

Pros: Liquidity, convenience, and easy inclusion in ISAs or SIPPs.

Cons: Ongoing management fees (0.2%–0.4%) and reliance on custodians.

Pros: Small minimum investment, instant buying/selling.

Cons: Dependence on provider integrity and storage verification.

Pros:Potential for higher returns when gold rises.

Cons: Company-specific and operational risks. Mining shares may fall even when bullion prices rise.

• Buy from reputable dealers approved by the London Bullion Market Association (LBMA).

• Check authenticity: look for hallmarks, assay certificates, and serial numbers.

• Storage: use professional vaulting services or insured home safes.

• Insurance: ensure full coverage against theft or loss.

• Digital holdings: verify that your provider segregates and allocates your gold under your name.

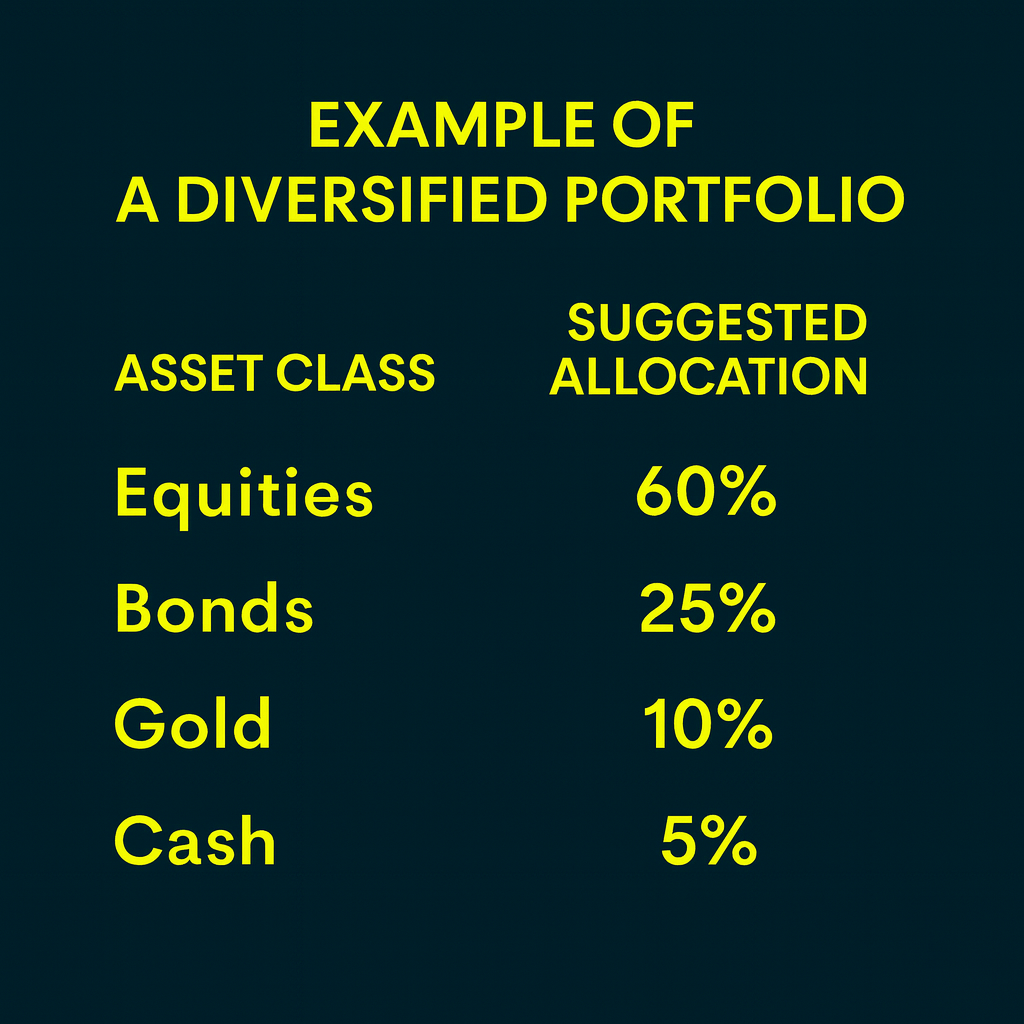

• Clarify your purpose: inflation hedge, diversification, or capital preservation.

• Choose your vehicle: physical, ETF, or digital.

• Start small: test your comfort with volatility.

• Select trusted providers: FCA-regulated or LBMA-accredited.

• Monitor performance: track gold against inflation and other assets.

• Blend with your overall plan: gold should support, not dominate, your strategy.

Seamlessly manage your finances, invest smarter, and achieve your financial goals with our cutting-edge solutions.

Subscribe to our newsletter for exclusive tips, expert advice, and the latest updates from Zomi Wealth—delivered straight to your inbox.

“Zomi Wealth’’ is a trading name of Zomi Group Limited who are authorised and regulated by the Financial Conduct Authority (FCA), FRN 149309. Past performance is not indicative of future returns. An investor may get back less than the amount invested. Information on past performance, where given, is not necessarily a guide to future performance. The capital value of units in the fund can fluctuate and the price of units can go down as well as up and is not guaranteed. The opinions and views expressed in this newsletter may not necessarily reflect the views of Zomi Group l Limited or its affiliates. The information provided in this newsletter is for informational purposes only and does not constitute a recommendation from any Zomi Group Limited entity to the recipient. Zomi Group Limited is not providing any financial, economic, legal, investment, accounting, or tax advice through this newsletter or to its recipient. Certain information contained in this newsletter constitutes “forward-looking statements,” and there is no guarantee that these results will be achieved. Zomi Group Limited has no obligation to provide any updates or changes to the information in this newsletter. Zomi Group Limited always recommends that the recipient take independent financial advice. Alternative investments often engage in leverage and other investment practices that are extremely speculative and involve a high degree of risk. Such practices may increase the volatility of performance and the risk of investment loss, including the loss of the entire amount that is invested. These investments are usually highly illiquid and generally not transferable without the content of the sponsor.

Investing in cryptocurrency is highly speculative and involves significant risk to capital, as its value is extremely volatile and can fluctuate widely in short periods. It is not regulated by the Financial Conduct Authority, meaning investors may not have access to financial protections, including the Financial Services Compensation Scheme (FSCS) or the Financial Ombudsman Service. There is also a risk of loss from fraud, cybersecurity breaches, or operational failures within cryptocurrency platforms. Investors should carefully consider whether they can afford to lose the entirety of their investment.

Know more about Zomi Wealth, how we invest, our plans and how to be a part of Zomi Wealth. Contact Us!

Seamlessly manage your finances, invest smarter, and achieve your financial goals with our Zomi Wealth App.